Size Guide

Understanding Mylulusstore Sizing

Description

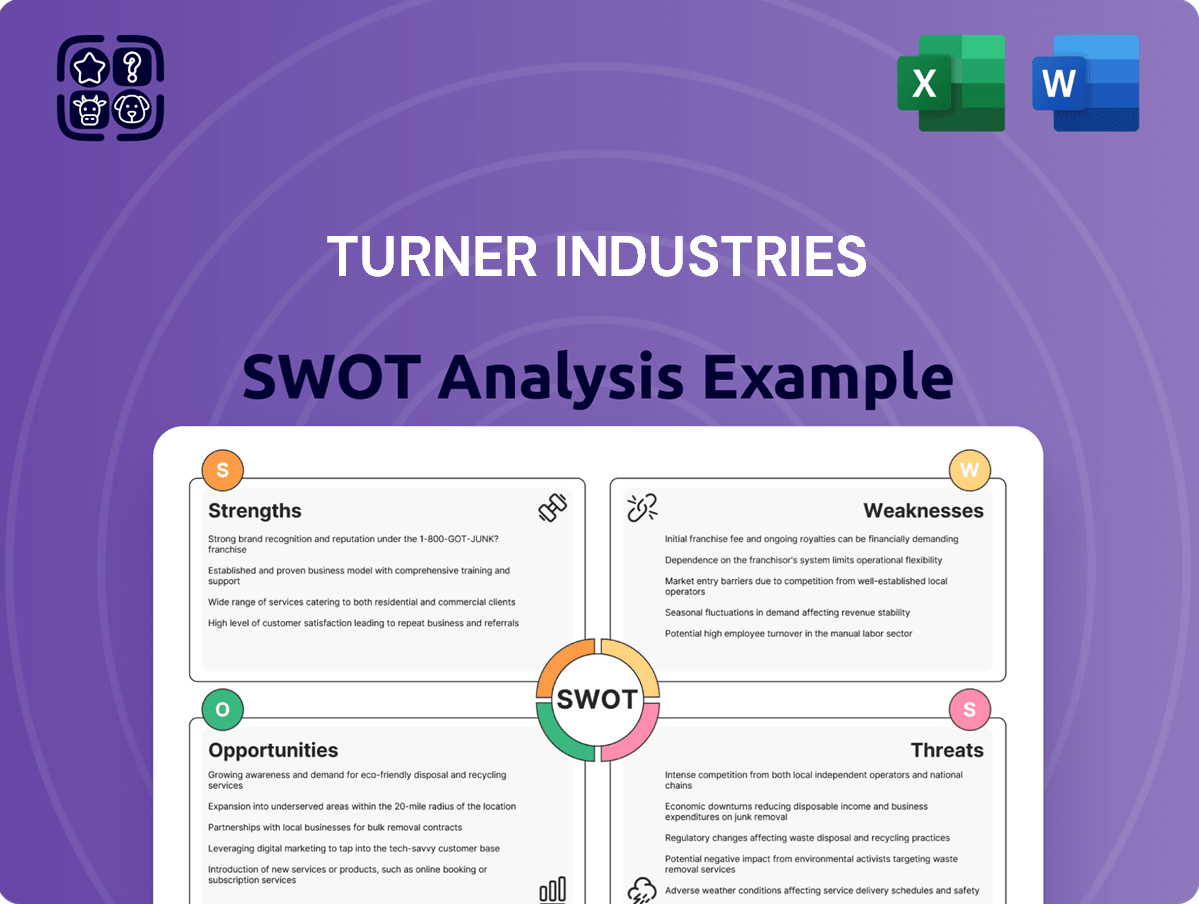

xYour Strategic Toolkit Starts Here

Turner Industries combines deep fabrication expertise and diverse industrial services with strong geographic reach, but faces cyclicality, labor constraints, and competitive pressure that could impact margins and growth.

Discover the full SWOT analysis to access a research-backed, editable report and Excel matrix—perfect for investors, advisors, and strategists who need actionable insights and ready-to-use deliverables.

Strengths

Comprehensive Single-Vendor Solution

Turner Industries offers a single-vendor model covering construction, fabrication, pipefitting, maintenance, and turnarounds, cutting client admin time and lowering multi-contractor logistics; in 2024 its integrated services supported projects worth over $1.1B, improving on-time delivery rates by ~12% and reducing subcontractor disputes by 30%, which boosts accountability and project synergy across the asset lifecycle.

Industry-Leading Safety Performance

Turner Industries runs the STEWARDS safety program and posts OSHA-recordable incident rates around 0.12 in 2024, far below the U.S. construction average ~1.8, making safety a key win when bidding major petrochemical and energy contracts. Clients cite safety as a primary selection criterion, so Turner’s zero-incident target reduces shutdown risks and protects client cashflows—loss avoidance that can equal millions per plant-day for large refineries.

Proprietary Project Management Technology

Turner uses proprietary tools like JIB.S and WinTake to cut estimation and execution time; in 2024 these systems helped reduce bid-to-award cycles by about 18% and trim average project cost overruns from 7.4% to roughly 3.1%.

Deep Regional Market Dominance

- Gulf Coast focus: ~55% of 2024 revenue (~$1.1bn)

- Year-end 2024 backlog: ~$1.3bn

- Long-term blue-chip clients: ExxonMobil, Shell, Chevron partners

- Regional density: faster mobilization, stronger regulatory knowledge

Extensive Specialized Fabrication Capacity

Turner Industries runs massive dedicated pipe and vessel fabrication plants that handled over $1.2 billion in shop-fabricated work in 2024, letting them do high-volume assembly in controlled conditions instead of on-site.

Modular fabrication cuts weather delays—shop work reduced schedule variance by ~18% in recent projects—and tightens quality control, lowering rework rates and boosting safety incident reduction.

Shipping finished modules globally improves delivery speed for large capital projects; Turner moved modules to 12 countries in 2024, supporting faster on-site hookup and lower installation labor.

- 2024 shop revenue: $1.2B

- Schedule variance cut: ~18%

- Modules shipped to 12 countries

- Lower rework and incident rates

Turner: Integrated single-vendor model drives $2B revenue, $1.3B backlog, 0.12 OSHA

Turner’s integrated single-vendor model, STEWARDS safety (OSHA-recordable ~0.12 in 2024), proprietary tools (bid-to-award -18%, overruns cut to ~3.1%), Gulf Coast concentration (~55% revenue ≈ $1.1B of $2.0B), 2024 backlog ~$1.3B, and $1.2B shop-fabrication drove faster mobilization, lower rework, and global module shipments (12 countries).

| Metric | 2024 |

|---|---|

| Total revenue | $2.0B |

| Gulf Coast rev | $1.1B (55%) |

| Backlog | $1.3B |

| Shop revenue | $1.2B |

| OSHA rate | 0.12 |

What is included in the product

Delivers a strategic overview of Turner Industries’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position and future growth.

Provides a concise SWOT matrix for Turner Industries to quickly align risk mitigation and growth initiatives across operations and project teams.

Weaknesses

High Sector Concentration

Turner Industries derives roughly 70–80% of revenue from oil, gas, and petrochemicals, leaving it exposed to energy cycles; for example, a 2020–2021 oil price slump cut industry capex by about 20–30% and similar shocks could quickly reduce Turner’s backlog.

Geographic Footprint Limitations

Turner Industries dominates the Gulf South but its physical footprint is concentrated, with over 60% of 2024 revenues tied to Louisiana and Texas operations, leaving it smaller vs global EPC peers with multinational revenue streams.

This regional reliance raises exposure to localized risks: 2020–2023 Gulf hurricanes caused estimated industry losses >$50bn, and oil price shocks can cut regional capital spending by 20%+ within 12 months.

Expanding to international or other US hubs needs large capex and faces high entry barriers—trade, local JV rules, labour unions—so diversification could take 3–7 years and hundreds of millions in investment.

Private Company Transparency Hurdles

High Sensitivity to Labor Costs

The business model depends on a large skilled workforce—welders, pipefitters, crane operators—making labor the biggest cost driver.

Wage inflation (US construction wages rose ~5.6% in 2024) and higher benefits push down margins if Turner Industries cannot pass costs to clients.

Keeping payroll, training, and contingent staffing scalable creates operational strain during demand swings.

- Labor-heavy: thousands of skilled trades

- Wage pressure: +5.6% (2024 US construction)

- Benefits add fixed costs

- High overhead for contingent staffing

Dependency on Mature Asset Maintenance

- ~60% services revenue from maintenance (2024 est.)

- Maintenance margins: mid-single digits; new-energy EPC: >12%

- Backlog stability via multi-year contracts >$50M

- Concentration risk vs growth in renewables, hydrogen

High oil/gas & Gulf South concentration fuels cyclical, hurricane and labor risks

Heavy exposure to oil/gas (70–80% revenue) and Gulf South concentration (60%+ of 2024 revenue in LA/TX) raise cyclical and localized risk; 2020–21 capex cuts of ~20–30% and 2020–23 hurricane losses >$50bn show impact. Private status limits capital-market access and benchmarking (68% public peers; 25–40% wider valuation ranges). Labor-heavy cost base faces wage inflation (~+5.6% in 2024) and maintenance-heavy revenue (~60%, mid-single-digit margins).

| Metric | Value (2024) |

|---|---|

| Oil/Gas revenue share | 70–80% |

| LA/TX revenue share | 60%+ |

| Maintenance services | ~60% |

| Wage inflation | +5.6% |

| Hurricane/industry losses (2020–23) | >$50bn |

Preview Before You Purchase

Turner Industries SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use immediately after checkout.

- Choosing a selection results in a full page refresh.